UK courier industry trends and strategies for 2026

- Andrew Buttrick

- May 4

- 8 min read

TL;DR:

UK courier industry growth is driven by e-commerce and industry consolidation but faces challenges like driver shortages, rising costs, and supply chain fragility. Sustainability mandates and customer expectations accelerate fleet electrification, with urban areas benefiting from flexible, low-emission delivery solutions. Technological adoption such as AI, parcel lockers, and micro-hubs is key to improving last-mile efficiency and resilience in competitive logistics environments.

The UK courier sector is posting strong growth numbers, and it is tempting to take those figures at face value. Revenue projected at £17.4bn for 2025, with 3 to 4% growth expected in 2026, suggests a healthy industry. But for business owners and logistics managers making real decisions about partnerships, fleets, and spending, headline figures only tell part of the story. The trends underneath those numbers, covering sustainability obligations, driver shortages, customer expectations, and supply chain fragility, are where strategy actually gets built or broken.

Table of Contents

Key Takeaways

Point | Details |

Moderate but stable growth | The UK courier industry is expanding with 3-4% annual growth, powered by parcel demand and consolidation. |

Sustainability drives investment | Electric fleets and green practices are essential for compliance and meeting rising customer expectations. |

Tech and people balance | AI, automation, and workforce strategies are equally crucial for fast, reliable deliveries and cost control. |

Resilience outperforms scale | Risk diversification, regional hubs, and agile partnerships offer greater security than growth alone. |

Market outlook and financial forecasts for 2026

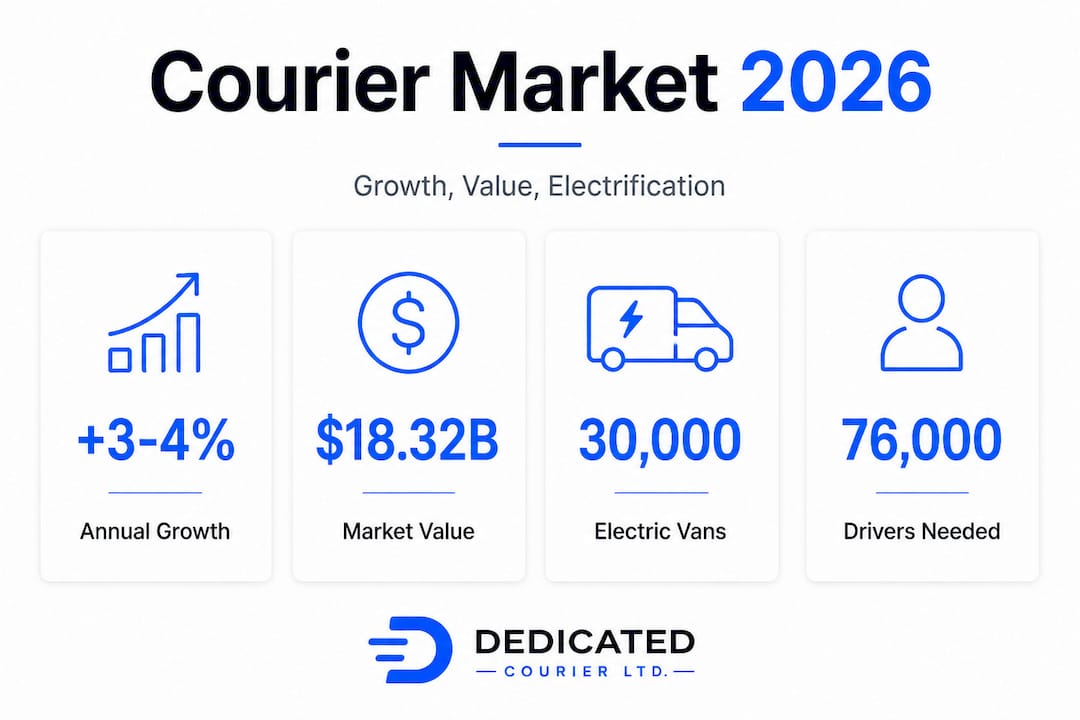

The UK courier, express, and parcel market is substantial and expanding. The CEP market valued at USD 17.77bn in 2025 is projected to reach USD 18.32bn in 2026, on a trajectory to USD 21.35bn by 2031 at a compound annual growth rate of 3.11%. When you factor in the broader postal and logistics ecosystem, IBISWorld projects the UK Postal and Courier industry at £30.3bn in 2026 following 1.3% growth in 2025 to 2026.

Metric | 2025 estimate | 2026 projection |

UK CEP market value | USD 17.77bn | USD 18.32bn |

UK Postal and Courier industry | £29.9bn | £30.3bn |

Projected CEP CAGR (to 2031) | 3.11% | 3.11% |

UK courier and parcel revenue | £17.4bn | +3 to 4% growth |

The primary growth engines are e-commerce expansion, rising parcel volumes per household, and ongoing consolidation among operators. Understanding how courier services drive retail success in this environment is increasingly important for any business managing outbound logistics. Letter volumes, by contrast, continue their long decline, with consumers and businesses shifting decisively to digital communication.

The risks attached to this growth are worth naming directly. Margin pressure from rising fuel, labour, and compliance costs is real. Smaller operators face competitive disadvantage without scale. Market consolidation benefits large players, but it can create reliability gaps for businesses that depend on agile, reliable courier services for time-sensitive deliveries.

Sustainability, electrification, and cost management

Sustainability is no longer optional for courier operators. Regulatory pressure, city clean air zones, and customer expectations are forcing decisions about fleet composition that have direct financial consequences.

Electric van registrations are expected to reach nearly 30,000 in 2025, a 9.4% increase on the prior year. Government incentives are supporting fleet electrification, but the upfront cost difference remains significant, averaging around £5,000 more per vehicle compared with a conventional petrol or diesel van. For fleets of any meaningful size, that capital outlay adds up quickly.

Factor | Petrol/diesel fleet | Electric fleet |

Upfront vehicle cost | Lower | £5,000 more per van |

Fuel and energy cost | Higher, volatile | Lower, more predictable |

Urban clean air zone charges | Applicable | Generally exempt |

Maintenance costs | Higher long-term | Lower long-term |

Customer sustainability demand | Not a differentiator | Growing competitive advantage |

The business case for electrification improves significantly over a three to five year horizon, particularly for urban and suburban delivery patterns. The challenge sits with rural operators, where charging infrastructure remains limited and range anxiety is a genuine operational concern. For those businesses, a hybrid approach, electrifying urban routes while retaining diesel capacity for rural coverage, is a practical middle ground. Understanding how net zero targets affect courier fleets is important for forward planning.

Pro Tip: Rather than purchasing electric vans outright, explore flexible EV leasing arrangements. These reduce upfront capital exposure and allow operators to upgrade to improved battery range as the technology matures, without being locked into today’s specifications.

Technology adoption: AI, automation, and the last-mile challenge

Technology is reshaping how deliveries are planned, executed, and tracked. The shift is accelerating, and businesses that fail to engage with it will find themselves at a growing disadvantage on cost and customer satisfaction.

Key technologies transforming delivery operations in 2026:

Machine learning for route optimisation processes traffic data, vehicle capacity, and delivery density in real time, cutting fuel use and improving drop rates per shift.

Dynamic driver allocation uses live demand signals to assign drivers based on proximity and availability, reducing dead mileage and improving responsiveness.

Parcel lockers and smart access points reduce the volume of failed first-time deliveries by giving recipients a secure, flexible collection option.

E-bikes and cargo bikes serve dense urban routes more efficiently than vans, particularly in areas with access restrictions or high congestion.

Micro-fulfilment hubs positioned on the edge of city centres allow faster, lower-cost last-mile dispatch for optimised courier logistics.

The scale of the failed delivery problem is not trivial. Failed first-time deliveries sit at 14% across the industry, and each failed attempt carries a direct cost in driver time, fuel, and administration. Customer expectations are also rising sharply: real-time tracking, narrow delivery slots, flexible re-delivery options, and carbon-aware choices are now standard requirements, not premium features.

“Customers in 2026 expect not just speed but control. They want to know where their parcel is, when it will arrive, and they want the option to redirect or reschedule without friction. Those that improve shipment logistics using technology will retain more customers.”

Pro Tip: Investing in parcel locker partnerships and integrating e-bike capacity for inner-city routes can reduce failed deliveries and lower per-delivery operating costs significantly, without requiring large capital investment in new vehicles.

Labour shortages and the future workforce

Technology can reduce dependency on drivers at the margins, but it cannot eliminate it. The sector faces a structural staffing problem that is not resolving quickly.

Labour shortages persist with an estimated need for 76,000 more drivers across the UK. The vacancy rate in transport roles is running at 4.1%, which means that for every 25 positions, roughly one remains unfilled at any given time. That sounds modest, but in an operation running tight schedules and high delivery volumes, even a small shortfall creates ripple effects on reliability and overtime spend.

The practical consequences for businesses contracting courier services include:

Longer lead times for booking, particularly at peak periods

Higher rates as operators pass on increased wage costs

Greater variability in service quality when temporary or agency drivers cover routes

Pressure on small and mid-sized operators who cannot match the salaries large networks offer

Pro Tip: Investing in driver satisfaction and retention, through transparent pay structures, route consistency, and access to benefits, reduces the cost and disruption of recruitment. The average cost of replacing a driver, when accounting for agency fees, onboarding, and lost productivity, is substantially higher than a modest pay increase to retain an experienced one.

Urban autonomous delivery trials are progressing, and some driverless last-mile pilots are underway in select city locations. However, widespread deployment remains years away from commercial scale. Rural areas face a different gap: the absence of EV charging infrastructure limits electrification in areas where driver recruitment is also most challenging.

Supply chain resilience: nearshoring, risk reduction, and strategic partnerships

Cost, technology, and labour pressures converge on a single question: how do you keep your supply chain moving when any one of those variables shifts unexpectedly?

The answer in 2026 centres on building resilience by design. Supply chain resilience through nearshoring, regional hub investment, multi-sourcing, and predictive analytics is the approach gaining traction among well-run logistics operations across Europe and the UK.

A practical approach to reducing supply chain risk:

Identify single points of failure in your current courier setup, whether that is one provider, one route, or one fulfilment location.

Build a multi-provider framework using both large network couriers for volume and specialist same-day providers for urgent or high-value items.

Establish regional holding points to reduce reliance on long-haul legs for time-sensitive goods.

Integrate predictive analytics to spot demand surges and potential disruption windows before they create service failures.

Review customs and cross-border documentation processes for any international lanes, as post-Brexit customs delays continue to average over two days for affected parcels.

“The businesses weathering supply chain disruption best in 2026 are those that treat logistics as a strategic function, not a cost line. Diversified partnerships and urgent shipment strategies aligned to risk profiles outperform single-supplier dependency every time.”

Post-Brexit complexities remain a real concern for businesses shipping internationally, and supply chain logistics planning should account for documentation, tariff classification, and border processing time as fixed variables, not exceptions.

A fresh take: What most courier strategies miss in 2026

Most of the industry conversation in 2026 is focused on scale and automation. That focus is understandable, but it creates a blind spot that smaller and mid-sized businesses can actually turn to their advantage.

The assumption that bigger networks and more automation always produce better outcomes for the customer is not consistently supported by experience. Large platforms introduce their own fragility: dependence on a single technology provider, reduced accountability when things go wrong, and limited flexibility for non-standard freight or urgent requirements. When a large network fails, it fails at volume.

Agility and niche specialisation frequently outperform scale for businesses with specific logistics needs. A manufacturer needing same-day delivery of a critical component does not need a parcel network optimised for high-volume e-commerce. They need a provider with real flexibility, direct communication, and proven courier reliability for urgent deliveries.

Overlooked strategies worth considering: cross-training logistics staff to cover multiple roles reduces operational vulnerability; hybrid urban and rural delivery models using different vehicle types reduce both cost and failed delivery rates; and investing in micro-hub relationships near key customer clusters cuts response time without large capital commitment.

The most future-ready logistics strategies in 2026 are not the ones chasing the largest automation budgets. They are the ones combining smart, appropriate technology with resilient, relationship-based operations that can flex when conditions change.

How Dedicated Sameday Courier can empower your business in 2026

The trends covered in this article point to one consistent conclusion: flexibility, speed, and reliability are non-negotiable for UK businesses managing time-sensitive logistics.

[

Dedicated Sameday Courier provides the kind of agile, dedicated delivery capacity that complements both large network relationships and standalone urgent requirements. The service operates 24/7, with a range of advanced courier vehicles suited to different freight types and volumes. Whether you need a single urgent collection or a structured programme of same-day deliveries, the nationwide sameday courier service is built to respond. Reach out via phone, email, or the online quote form to discuss how the service can be tailored to your 2026 logistics requirements.

Frequently asked questions

What is driving growth in the UK courier industry in 2026?

E-commerce expansion, rising parcel volumes, and industry consolidation are the main growth drivers, with 3 to 4% growth projected for the sector in 2026.

Why is fleet electrification important for courier firms in 2026?

Sustainability regulations, government incentives, and customer demand for low-carbon delivery are compelling operators to adopt electric vans, with registrations expected to reach 30,000 in 2025 alone.

How are customer expectations changing for courier services?

Customers now expect real-time tracking, flexible re-deliveries, narrow delivery slots, and carbon-aware delivery options as standard, not as premium add-ons.

What are the main risks facing UK courier businesses in 2026?

Labour shortages requiring 76,000 more drivers, a 4.1% vacancy rate, and supply chain disruption risks from single-provider dependency are the top concerns.

Will Brexit and international shipping delays still affect UK couriers in 2026?

Yes, post-Brexit customs delays continue to affect international parcels, with average wait times over two days for cross-border shipments, making accurate documentation and planning essential.

Recommended

Comments